How to Correctly Calculate GST on Air Tickets for Indian Travel Agencies

The 5% vs 18% split confuses most agents. Here's exactly how it works — with formulas, real scenarios, and how MoonTrip automates the entire calculation.

Direct Answer: How to Calculate Air GST

Enter the fare, choose the class, then either add GST or extract it from an inclusive fare.

GST = Base fare × 5 / 100

GST Amount = Base Fare × GST Rate / 100

Total Fare = Base Fare + GST Amount

If fare is already GST-inclusive:

GST Amount = Total Fare × GST Rate / (100 + GST Rate)

Base Fare = Total Fare - GST Amount

Use 5% for domestic economy and 12% for domestic business class.International Ticket Notes

Standalone international flight ticket:

GST = Base Fare × GST Rate / 100

Overseas tour programme package:

GST = calculate where applicable

TCS = handled separately under Income Tax rulesWhy Air GST Is Different from Standard GST

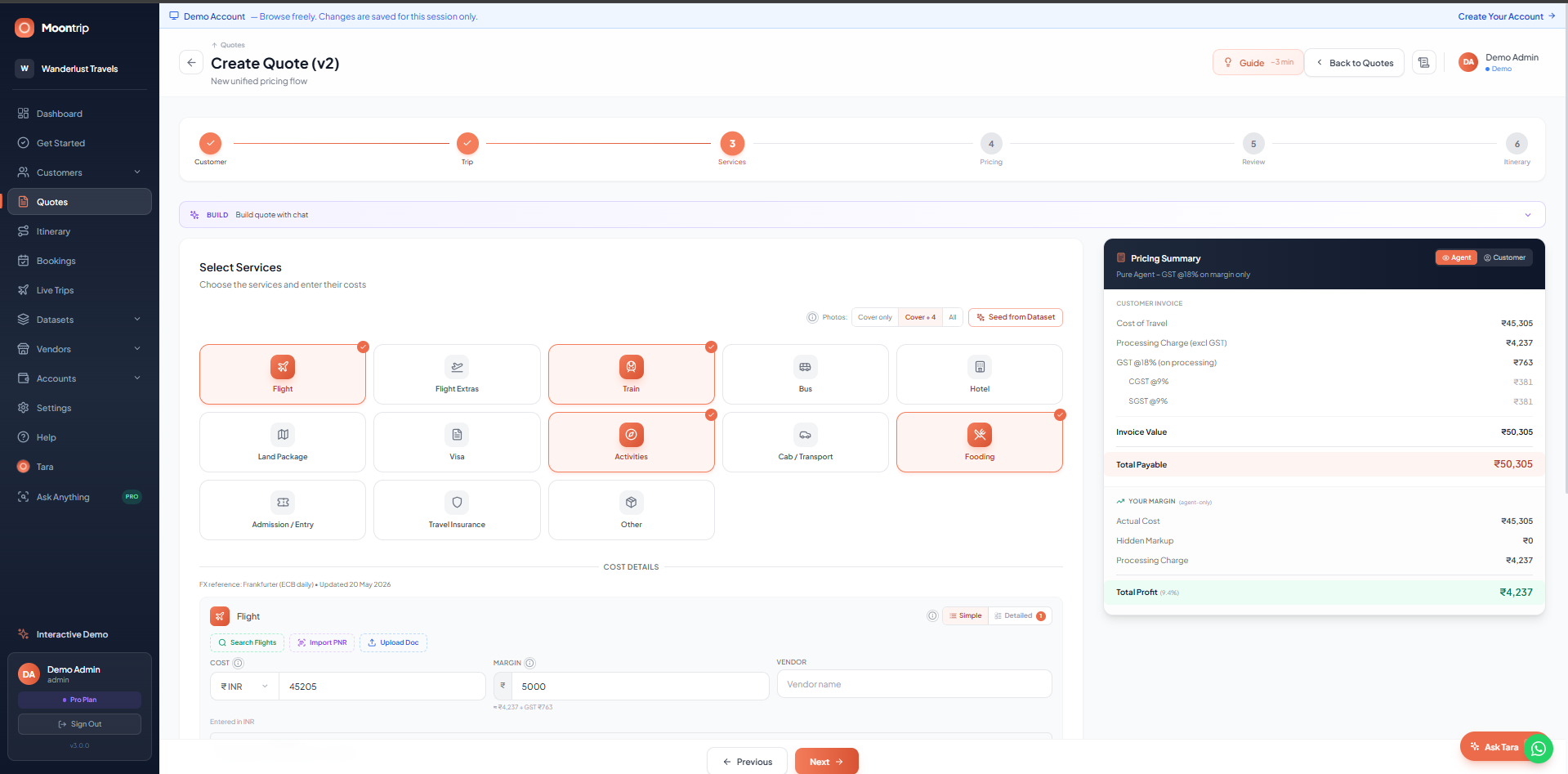

Most goods and services in India follow a single GST rate. Air tickets don't. Depending on how you source the ticket (GDS consolidator, LCC direct, or your own markup), the GST rate, the taxable value, and even the billing model change. Getting this wrong means incorrect GSTR-1 filings, ITC mismatches, and potential notices from the department.

Indian travel agencies typically deal with two billing models for air tickets — Pure Agent vs Principal — and each has its own GST treatment. The base fare is the airline-published ticket price before airport taxes and surcharges — and it is the only component subject to GST under the Principal model.

Scenario 1: GDS / IATA Net-Rate Tickets (Principal Model)

A GDS consolidator is a third-party service provider that supplies discounted air tickets at net rates to travel agents for resale. When a travel agent purchases a ticket at a net rate from a GDS consolidator (Amadeus, Sabre, Galileo) or directly through IATA, the agent is acting as a Principal — buying and reselling the ticket.

How the Tax Works

- •GST Rate: 5% on the base fare (no Input Tax Credit available)

- •Taxable Value: The base fare of the ticket (excluding airport taxes like YQ, YR, PSF, UDF)

- •What the customer sees: Total ticket price + 5% GST on base fare

Base Fare = ₹5,000

Airport Taxes (YQ) = ₹2,500

GST @5% = ₹5,000 × 5% = ₹250

Customer Invoice = ₹5,000 + ₹2,500 + ₹250 = ₹7,750

CGST = ₹125 | SGST = ₹125 (intra-state)

— or —

IGST = ₹250 (inter-state)

Scenario 2: LCC / Standard Booking (Pure Agent Model)

When a travel agent books a ticket on behalf of a customer from a low-cost carrier (IndiGo, SpiceJet, Air India Express) or any airline where the agent earns a commission or charges a service fee, the agent is acting as a Pure Agent.

How the Tax Works

- •GST Rate: 18% — but only on the service fee / commission, not the ticket price

- •Taxable Value: Only the agent's service fee or processing charge

- •Ticket cost: Passed through as a reimbursement (not taxable under Pure Agent)

Ticket Cost (reimbursement) = ₹4,200

Agent Service Fee = ₹500

GST @18% on Service Fee = ₹500 × 18% = ₹90

Customer Invoice = ₹4,200 + ₹500 + ₹90 = ₹4,790

CGST = ₹45 | SGST = ₹45 (intra-state)

— or —

IGST = ₹90 (inter-state)

Scenario 3: Agent Charges a Markup Over the Ticket

Some agents add a markup to the ticket price rather than a transparent service fee. In this case, the billing model determines the GST treatment:

Vendor Net Rate = ₹5,000

Agent Markup = ₹800

Selling Price = ₹5,800

GST @5% = ₹5,800 × 5% = ₹290

Customer pays = ₹5,800 + Airport Taxes + ₹290Ticket at Cost = ₹5,000 (reimbursement — no GST)

Processing Charge = ₹800 (this IS the markup, shown as fee)

GST @18% = ₹800 × 18% = ₹144

Customer pays = ₹5,000 + Airport Taxes + ₹800 + ₹144CGST/SGST vs IGST: The State Split

GST is further split based on whether the transaction is intra-state or inter-state:

- •Intra-state (agency and customer in same state): GST is split equally into CGST + SGST. E.g., 18% = 9% CGST + 9% SGST

- •Inter-state (different states): Full rate charged as IGST. E.g., 18% IGST

- •Determination: Based on the Place of Supply rules — the state of the customer's GSTIN (B2B) or the agency's location (B2C)

Service Fee = ₹500, GST Rate = 18%

Intra-state (same state):

CGST = ₹500 × 9% = ₹45

SGST = ₹500 × 9% = ₹45

Inter-state (different states):

IGST = ₹500 × 18% = ₹90Tax Collected at Source (TCS) is separate from GST and applies to overseas tour programme packages, not to every standalone international ticket. From 1 Apr 2026, the top-line TCS rate on an overseas tour programme package is 2% from the first rupee. If the customer buys only an international ticket or only a hotel stay, it is not treated as an overseas tour programme package; a qualifying package includes at least two travel components such as ticket plus hotel, boarding, lodging, or similar related expenditure.

Base Fare = ₹25,000

Airport Taxes = ₹8,000

GST @5% = ₹25,000 × 5% = ₹1,250

TCS @2% = (₹25,000 + ₹8,000) × 2% = ₹660

Customer Invoice = ₹25,000 + ₹8,000 + ₹1,250 + ₹660 = ₹34,910The Manual Way vs The MoonTrip Way

The Manual Spreadsheet Approach

To calculate Air GST manually, a travel agent must:

- •Identify whether the ticket is GDS net-rate or LCC/commission-based

- •Separate base fare from airport taxes (YQ, YR, PSF, UDF, K3)

- •Determine the billing model (Pure Agent vs Principal)

- •Apply the correct GST rate (5% on base fare OR 18% on service fee)

- •Check the customer's GSTIN to determine CGST/SGST vs IGST split

- •Add TCS if international and applicable

- •Categorize as B2B or B2C for GSTR-1 filing

- •Track the service fee separately for Input Tax Credit claims

GSTR-1 and GSTR-3B: How Air Tickets Appear

In your GST returns, air ticket transactions appear differently based on the billing model:

- •GSTR-1 (Outward Supply): B2B invoices with customer GSTIN appear in Table 4A. B2C invoices appear in Table 7/8 based on invoice value. HSN/SAC code 996411 for air transport services.

- •GSTR-3B (Summary Return): Total taxable value, CGST, SGST, IGST reported in Table 3.1. Pure Agent reimbursements are excluded from taxable turnover.

- •Input Tax Credit: Under Principal @5%, no ITC is available. Under Pure Agent @18%, ITC can be claimed on the GST paid on your service fee-related expenses.

Air GST FAQ

How do I calculate air GST?

Calculate air GST by multiplying the base fare by the applicable GST rate and dividing by 100. Domestic economy flight tickets attract 5% GST, while domestic business class flight tickets attract 12% GST.

GST amount = Base fare × GST rate / 100How to calculate GST if flight fare is inclusive of GST?

If the flight fare already includes GST, extract the tax from the total using the inclusive formula. For an economy fare at 5%, multiply the total fare by 5 and divide by 105. For a business class fare at 12%, multiply the total fare by 12 and divide by 112.

GST = Total × rate / (100 + rate)What is GST on economy vs business class flight tickets?

Domestic economy flight tickets attract 5% GST. Domestic business class flight tickets attract 12% GST. A travel agency may also need to apply a separate GST rule on service fees, commissions, or markups depending on whether the booking is handled as Principal or Pure Agent.

How do travel agents calculate GST on air tickets?

Travel agents first identify the billing model. Under the Principal model, GST is generally calculated on the base fare. Under the Pure Agent model, GST is calculated only on the service fee or commission, not on the reimbursed ticket cost. The billing model decides whether GST applies on the base fare or only on the service fee.

Related Guides

Stop calculating manually

MoonTrip automates GST, invoicing, and profit tracking for Indian travel agencies.

Get Started Free