How MoonTrip Automates GSTR-1 and GSTR-3B Filing Data for Indian Travel Agencies

B2B vs B2C categorization, travel-specific HSN/SAC codes, CGST/SGST/IGST split, credit note adjustments — all automated. Stop filing GST returns manually.

Why GST Filing Is Painful for Travel Agencies

Travel agencies don't sell one type of product at one GST rate. A single booking can include flights (SAC 996411), hotels (SAC 996311), cab transfers (SAC 996422), and a processing charge (SAC 998551) — each with its own tax treatment. Multiply that by 50-100 bookings per month, add cancellation credit notes, and you have a filing nightmare.

Most agents spend 2-3 days every month compiling data from invoices, spreadsheets, and bank statements to prepare their GSTR-1 and GSTR-3B returns. Errors lead to notices, penalties, and ITC mismatches that take months to resolve.

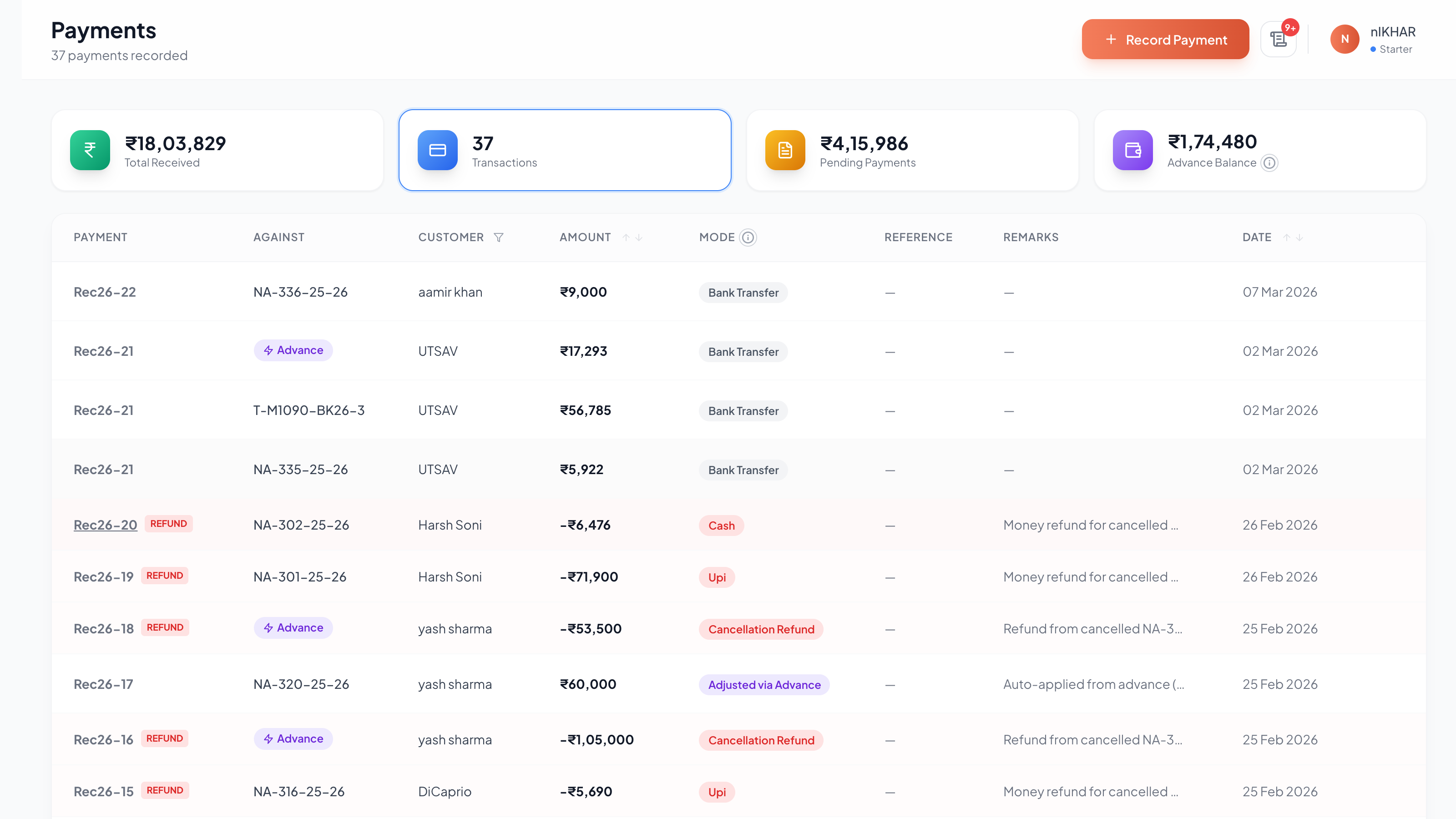

GSTR-1: The Detailed Invoice Return

GSTR-1 is the monthly outward supply return filed with GST authorities, detailing every invoice issued by the travel agency with customer GSTIN, HSN/SAC codes, and tax breakdowns. It requires invoice-level detail categorized into specific tables.

Table 4A: B2B Invoices (Registered Customers)

Every invoice issued to a customer with a valid GSTIN goes here. Required fields:

- •Customer GSTIN: 15-character alphanumeric (e.g., 27AABCT1234F1Z5)

- •Invoice Number & Date

- •Invoice Value: Total including GST

- •Taxable Value: Amount on which GST is calculated

- •Tax Breakup: CGST, SGST, IGST amounts separately

- •Place of Supply: 2-digit state code (derived from customer GSTIN)

- •Reverse Charge: Yes/No flag

| Field | Value |

|---|---|

| Customer GSTIN | 29AABCT5678G1Z2 (Karnataka) |

| Invoice No. | BK-M1090-26-42 |

| Invoice Date | 10-Mar-2026 |

| Invoice Value | ₹89,130 |

| Place of Supply | 29 — Karnataka |

| Reverse Charge | No |

| Taxable ValueProcessing Charge — Pure Agent | ₹3,500 |

| IGSTInter-state: agency in MH, customer in KA | ₹630 |

| CGST | ₹0 |

| SGST | ₹0 |

Under Pure Agent, only the processing charge is taxable — reimbursement costs are excluded from turnover.

Table 5: B2B Large Invoices (B2C over ₹2.5 Lakh)

Inter-state B2C invoices exceeding ₹2.5 lakh in value are reported individually with Place of Supply details.

Table 7: B2C Others (Unregistered Customers)

All remaining B2C invoices (individual customers without GSTIN) are reported as aggregated totals — grouped by tax rate. No individual invoice details needed.

| Tax Rate | Taxable Value | CGST | SGST | Description |

|---|---|---|---|---|

| 18% (Intra-state) | ₹47,500 | ₹4,275 | ₹4,275 | B2C processing fees |

| 5% (Intra-state) | ₹1,20,000 | ₹3,000 | ₹3,000 | B2C flight base fares |

Table 9B: Credit Notes (Cancellations & Refunds)

Every cancellation note and credit note issued during the period is reported here. This reduces your output tax liability for the month.

| Field | Value |

|---|---|

| Original Invoice | BK-M1090-26-38 (₹1,20,000) |

| Credit Note No. | CN-2026-0015 |

| CN Date | 20-Mar-2026 |

| CN ValueReversal after ₹30,000 cancellation charges | ₹90,000 |

| Tax | Original | Reversal |

|---|---|---|

| CGST | ₹9,000 | ₹6,300 |

| SGST | ₹9,000 | ₹6,300 |

| Total | ₹18,000 | ₹12,600 |

Net effect: Reduces your March GSTR-1 output by ₹12,600 in tax.

GSTR-3B: The Monthly Summary Return

GSTR-3B is the monthly summary GST return showing aggregate outward supplies, input tax credits claimed, and net tax liability payable. Unlike GSTR-1, it doesn't need invoice-level detail — just aggregated numbers. But getting those numbers right requires accurate data from every invoice and credit note.

Table 3.1: Outward Supplies

| Category | Taxable Value | IGST | CGST | SGST |

|---|---|---|---|---|

| (a) Outward taxable supplies | ₹2,85,000 | ₹18,630 | ₹12,150 | ₹12,150 |

| (b) Zero-rated supplies | ₹0 | — | — | — |

| (c) Nil / Exempt supplies | ₹0 | — | — | — |

| (d) Inward supplies (RCM) | ₹0 | — | — | — |

Table 4: Input Tax Credit (ITC)

Under the Principal model, travel agents can claim ITC on GST paid to vendors. Under Pure Agent, vendor costs are reimbursements — no ITC on those, but ITC on operational expenses (rent, software, etc.) is claimable.

| Metric | Principal @18% | Pure Agent |

|---|---|---|

| GST paid to vendor | ₹8,370 | N/A (reimbursement) |

| GST charged to customer | ₹11,160 | ₹450 (on service fee) |

| ITC Claim | ₹8,370 | ₹200 (operational) |

| Net GST Payable | ₹2,790 | ₹250 |

HSN/SAC Codes for Travel Services

An HSN/SAC code is a government-mandated classification code for goods (HSN) or services (SAC) required on every GST invoice. Travel agencies deal exclusively with SAC codes. Using the wrong code can trigger notices during GST audits.

| Service | SAC Code | GST Rate |

|---|---|---|

| Air Transport | 996411 | 5% (Principal) / 18% (Pure Agent fee) |

| Hotel Accommodation | 996311 | 12% or 18% (based on room tariff) |

| Railway Transport | 996421 | 5% |

| Bus / Cab Services | 996422 | 5% or 18% |

| Activities / Amusement | 998555 | 18% |

| Insurance Services | 997159 | 18% |

| Visa / Professional | 998559 | 18% |

| Tour Operator Processing | 998551 | 18% |

| Land Packages | 998559 | 5% (tour package) or 18% |

CGST/SGST vs IGST: Automatic State-Based Split

The GST split depends on whether the supply is intra-state or inter-state:

Agency GSTIN: 27AABCT1234F1Z5 → State: 27 (Maharashtra)

Customer A GSTIN: 27XXXXX → State: 27 (Maharashtra)

→ Same state → INTRA-STATE

→ GST 18% = CGST 9% + SGST 9%

Customer B GSTIN: 29XXXXX → State: 29 (Karnataka)

→ Different state → INTER-STATE

→ GST 18% = IGST 18%

Customer C (No GSTIN, Individual):

→ B2C → Use agency's state as Place of Supply

→ GST 18% = CGST 9% + SGST 9%

International Client (Place of Supply = 99):

→ Export of services → Zero-rated / No GSTMoonTrip derives the state code from the first 2 digits of the customer's GSTIN automatically. For B2C customers without GSTIN, the agency's state is used as the Place of Supply. This determination drives the correct split across every invoice.

How Pure Agent vs Principal Affects Your Returns

The billing model fundamentally changes what appears in your GSTR-1 and GSTR-3B:

Pure Agent Model

Booking Total (customer pays) = ₹89,130

Reimbursement Costs = ₹85,000 ← NOT in GSTR turnover

Processing Charge (taxable) = ₹3,500 ← This is your GSTR-1 entry

GST @18% on Processing Charge = ₹630

GSTR-1 Taxable Value = ₹3,500 (not ₹89,130!)

GSTR-3B Turnover = ₹3,500

Your tax liability = ₹630Principal Model (@18%)

Booking Total (customer pays) = ₹73,160

Package Price (taxable) = ₹62,000 ← Full amount in GSTR

GST @18% on Package Price = ₹11,160

Vendor GST (ITC claimable) = ₹8,370

GSTR-1 Taxable Value = ₹62,000

GSTR-3B Turnover = ₹62,000

Gross tax liability = ₹11,160

ITC = ₹8,370

Net tax payable = ₹2,790Principal Model (@5% Tour Package)

Booking Total (customer pays) = ₹65,100

Package Price (taxable) = ₹62,000

GST @5% on Package Price = ₹3,100

ITC = NOT available under 5% scheme

GSTR-1 Taxable Value = ₹62,000

GSTR-3B Turnover = ₹62,000

Net tax payable = ₹3,100 (no ITC offset)TCS on International Packages

For international tour packages, travel agents must collect Tax Collected at Source (TCS) at 5% under Section 206C(1G) of the Income Tax Act. This applies when the total remittance under LRS exceeds ₹7 lakh in a financial year.

International Package = ₹2,50,000

GST @5% (tour package) = ₹12,500

TCS @5% on package value = ₹12,500

Customer Pays = ₹2,50,000 + ₹12,500 + ₹12,500 = ₹2,75,000

GSTR Reporting:

Taxable Value = ₹2,50,000

GST = ₹12,500

TCS Reporting (separate):

TCS collected = ₹12,500

To be deposited with IT department

Reflected in Form 27EQ

Note: TCS is NOT part of GST — it's Income Tax.

MoonTrip tracks both separately.The Complete Monthly Filing Flow

Here's what a month-end GST filing cycle looks like with MoonTrip:

| GSTR-1 Table | Detail | Taxable Value |

|---|---|---|

| Table 4A (B2B) | 12 invoices | ₹1,85,000 |

| Table 7 (B2C) | 38 invoices | ₹95,000 |

| Table 9B (CN) | 3 credit notes | −₹42,000 |

| Table 12 (HSN) | SAC-wise summary | Auto-grouped |

| Item | Amount |

|---|---|

| Outward Supplies | ₹2,38,000 |

| IGST | ₹15,200 |

| CGST | ₹10,800 |

| SGST | ₹10,800 |

| ITC Claimed | −₹8,370 |

| Net GST Payable | ₹28,430 |

What MoonTrip Automates vs What You Still Do

Fully Automated by MoonTrip

- •SAC code assignment: Every line item tagged with the correct code (996411, 996311, 996422, etc.)

- •B2B vs B2C categorization: Based on customer GSTIN — corporate with GSTIN = B2B, individual without = B2C

- •CGST/SGST vs IGST split: Derived from customer GSTIN state code vs agency state code

- •Place of Supply determination: First 2 digits of customer GSTIN, or agency state for B2C

- •Credit note tracking: Every cancellation note linked to original invoice with tax reversal amounts

- •Dual invoice tax separation: Customer invoice GST vs internal margin invoice GST tracked separately

- •TCS calculation: Auto-applied on international packages with separate tracking

- •Pure Agent exclusion: Reimbursement costs automatically excluded from taxable turnover

What You Do

- •Export the data: Download the GSTR-1/3B summary from MoonTrip

- •Upload to GST portal: Submit the data via the government's GST portal or offline utility

- •Review and file: Verify the numbers and file the return

Common GSTR Mistakes Travel Agents Make

- •Including reimbursements in turnover: Under Pure Agent, vendor costs are not your supply — they shouldn't appear in GSTR-1 taxable value. Including them inflates your turnover and tax liability.

- •Wrong SAC codes: Using a generic "998599" for everything instead of specific codes (996411 for flights, 996311 for hotels). This triggers HSN mismatch notices.

- •Missing credit notes: Forgetting to report cancellation credit notes in Table 9B. This means you're paying tax on revenue you've already refunded.

- •IGST vs CGST/SGST errors: Applying CGST+SGST on an inter-state supply or IGST on an intra-state supply. Both create filing mismatches that are flagged during reconciliation.

- •Not claiming ITC under Principal: If you're using the Principal model, you're entitled to ITC on vendor GST. Many agents forget to claim this, paying more tax than necessary.

- •TCS mixed with GST: TCS is Income Tax, not GST. It should not appear in GSTR-1 or GSTR-3B. Mixing the two creates reconciliation nightmares.

Related Guides

Stop calculating manually

MoonTrip automates GST, invoicing, and profit tracking for Indian travel agencies.

Get Started Free